When it comes to financial planning, insurance plays a key role in protecting your family’s future. One popular option is whole life insurance, a form of permanent life insurance that offers both a death benefit and a savings component. But what exactly is whole life insurance, and how does it differ from other types of insurance? Let's dive in and explore everything you need to know about whole life insurance.

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance designed to provide coverage for your entire life, as long as premiums are paid. Unlike term life insurance, which only provides coverage for a specific period (like 10, 20, or 30 years), whole life insurance guarantees a payout whenever you pass away. This makes it an attractive option for individuals who want lifelong coverage and a predictable death benefit for their beneficiaries.

Additionally, whole life insurance comes with a cash value component, which makes it stand out. Over time, a portion of your premiums builds up as cash value, which grows on a tax-deferred basis. You can borrow against this cash value, withdraw it, or even use it to pay premiums.

Key Features of Whole Life Insurance

- Lifelong Coverage: Whole life insurance offers permanent coverage, meaning the policy doesn’t expire as long as you continue to pay the premiums. This guarantees financial protection for your beneficiaries whenever you pass away.

- Fixed Premiums: One of the most appealing aspects of whole life insurance is its fixed premiums. Unlike other types of insurance where premiums can increase over time, whole life premiums remain constant throughout the life of the policy. This can provide a sense of financial stability since your payments won’t change, even as you age.

- Cash Value Accumulation: The cash value component of whole life insurance is an investment element that grows over time. It accumulates tax-deferred, which means you won’t owe taxes on the growth until you withdraw the funds. You can access this cash value during your lifetime by taking a loan against it or making a withdrawal, giving you financial flexibility.

- Dividends: Some whole life policies are participating policies, which means the insurance company may pay you dividends based on its financial performance. You can use these dividends to increase your policy's cash value, purchase additional coverage, or even reduce your premium payments.

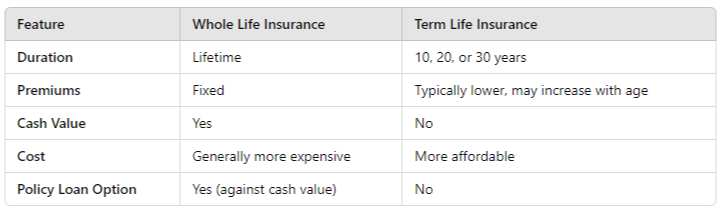

Whole Life vs. Term Life Insurance

The primary distinction between whole life and term life insurance is the duration of coverage. Term life provides coverage for a set number of years, often at a lower cost than whole life, but it does not build cash value and expires if you outlive the policy term. Whole life, on the other hand, is designed to cover you for your entire life and includes the added benefit of cash value accumulation.

Here’s a quick comparison:

Pros and Cons of Whole Life Insurance

Like any financial product, whole life insurance has its advantages and disadvantages.

Pros:

- Guaranteed death benefit: Your beneficiaries will receive a payout regardless of when you pass away.

- Fixed premiums: You can budget with confidence, knowing your premiums won’t increase.

- Cash value: The ability to accumulate savings and potentially borrow from the policy offers added financial flexibility.

- Tax advantages: The cash value grows tax-deferred, and the death benefit is typically tax-free for beneficiaries.

Cons:

- Higher premiums: Whole life insurance is significantly more expensive than term life insurance for the same level of coverage.

- Complexity: Whole life policies can be more difficult to understand, especially when it comes to the cash value and dividends.

- Lower return on investment: The investment component of whole life insurance may not offer as high of a return compared to other investment options.

When Does Whole Life Insurance Make Sense?

Whole life insurance is often recommended for individuals who want lifetime coverage and are looking for a way to build savings through their policy. It can also be a good choice for those who have maxed out their other tax-advantaged accounts (like IRAs and 401(k)s) and are looking for an additional way to grow wealth tax-deferred.

It’s particularly useful for:

- Wealth transfer: If you want to ensure a legacy for your heirs, whole life can provide a guaranteed payout regardless of when you die.

- Estate planning: The death benefit can help cover estate taxes or provide liquidity to your beneficiaries.

- Business owners: Whole life can be used for buy-sell agreements or to ensure the continuation of a business after an owner passes away.

Whole life insurance offers lifelong protection and a cash value component, making it a versatile financial tool. However, it’s important to weigh the higher cost and complexity against your individual needs. For those who want lifetime coverage, guaranteed death benefits, and the potential to build savings, whole life insurance can be an excellent addition to your financial plan.

If you're unsure if whole life insurance is the right fit, it's a good idea to consult with a financial advisor who can assess your personal goals and recommend the best type of policy for your needs. If you are interested in learning more, get started with us here.

Material discussed is meant for general informational purposes only and is not to be construed as tax, legal, or investment advice. Although the information has been gathered from sources believed to be reliable, please note that individual situations can vary. Therefore, the information should be relied upon only when coordinated with individual professional advice.

All whole life insurance policy guarantees are subject to the timely payment of all required premiums and the claims paying ability of the issuing insurance company. Policy loans and withdrawals affect the guarantees by reducing the policy’s death benefit and cash values.

Some whole life polices do not have cash values in the first two years of the policy and don’t pay a dividend until the policy’s third year. Talk to your financial representative and refer to your individual whole life policy illustration for more information.